Handbook on Employee Stock Options (ESOPs)

Employee Ownership is a relatively new concept in the Indian ecosystem. However, startups in India are embracing this concept and are looking out for ways to incentivize their workforce. Grant of employee stock options (ESOPs) to the employees is one of the ways to promote the sense of ownership in the employees.

Employee Stock Options (ESOPs) are the options given to the permanent employees of a company which gives them the right to purchase the shares of the company, in future, at a pre-determined price.

Concept underlying ESOPs

In order to reward its employees and to give them a sense of ownership, companies include ESOPs in their compensation structure. ESOPs give an option to the employees to acquire the shares of the company in future at a discounted value (“exercise price”). There are certain conditions which have to be fulfilled by the employee in order to get the right to convert the ESOP options into shares (also known as “vesting”). There shall be a minimum period of one year between the grant of options and vesting of option (also known as “cliff period”). Once the options get vested in an employee, the employee can exercise their right to convert the vested options into shares by paying the exercise price for the vested options and also the income tax liability on the notional income (on account of difference in fair market value (FMV) of shares and the exercise price). FMV is assessed on the basis of valuation certificate granted by a merchant banker. The employer can specify a period after vesting during which the ESOPs have to be converted to shares. (“Exercise Period”)

From the standpoint of liquidity, ESOPs can be bought back by the employer even before they are converted into shares. Alternatively, employees can be provided an option to sell their shares to the investors at the time of fundraising. The shares can also be sold at the time of IPO or after the company is listed.

Who all can be granted ESOPs?

ESOPs can be granted to the directors, officers or employees of a company or of its holding company or subsidiary company or companies, if any.

ESOPs cannot be granted to

- a promoter or a person belonging to the promoter group

- a director holding directly or indirectly more than 10 per cent of the equity shares

- an independent director

- a temporary employee or a freelancer

However, a startup company can grant ESOPs to promoters and directors holding more than 10% of equity shares up to ten (10) years of its incorporation.

Applicable Laws and Regulations

Section 62(1) of the Companies Act, 2013 provides that a company can issue ESOPs to its employees under a scheme approved by its shareholders through a special resolution passed by the company.

Unlisted Companies. Rule 12 of the Companies (Share Capital and Debentures) Rules 2014 provides detailed guidelines which needs to be followed by the companies while granting ESOPs.

Listed Companies. Securities and Exchange Board of India (Share Based Employee Benefits) Regulations, 2014 have to be complied by the listed companies.

Accounting. Any company implementing ESOPs shall follow the requirements of the

- Ind AS 102 – Accounting for Share Based Payments (if company is following Companies (Indian Accounting Standards) Rules, 2015)

- ‘Guidance Note on Accounting for Share-based Payments’ issued by the Institute of Chartered Accountants of India (ICAI) (if company is following Accounting Standards under Companies (Accounting Standards) Rules, 2006)

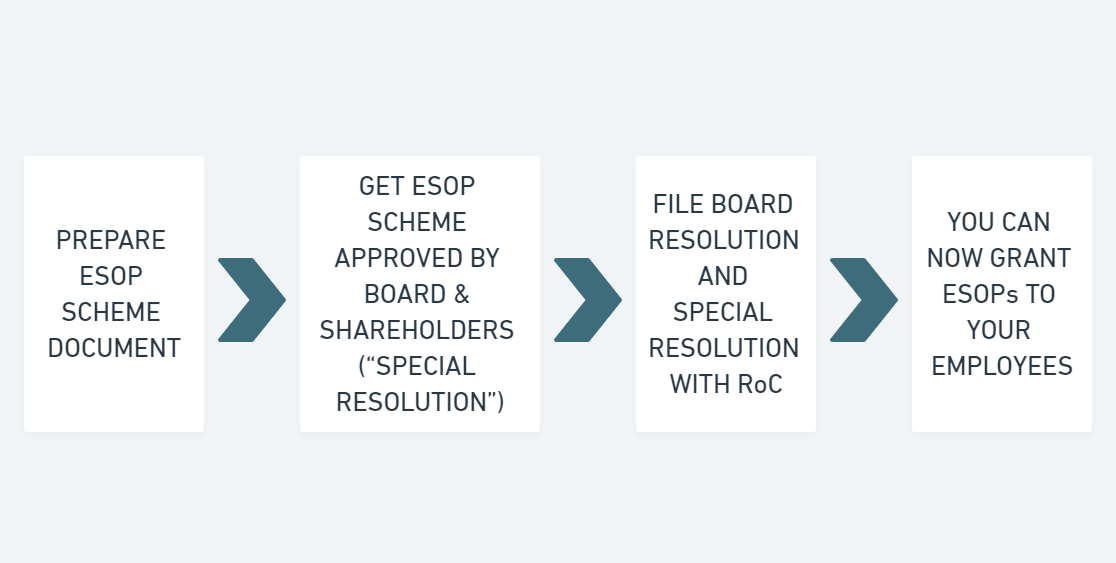

Procedure to grant ESOPs

- The company needs to get the ESOP scheme prepared. It is advisable to get the scheme document prepared through or vetted by a lawyer.

- ESOP scheme needs to be approved by the Board and also by the shareholders through a special resolution. Board resolutions and the special resolution has to be filed with Registrar of Companies (ROC) using MGT Form 14.

- ESOPs can now be granted to the employees by way of a grant letter.

- The company needs to maintain a register in the format of Form No. SH.6 and the particulars of ESOPs granted by the company have to be recorded in this register forthwith. The entries in the register have to be authenticated by a Company Secretary.

- The company needs to report the important details about grant of ESOPs in the Directors’ Report.

Mandatory Compliances

- The issue of Employees Stock Option Scheme has to be approved by the shareholders of the company by passing a special resolution (number of votes cast in favour of the resolution shall not be less than three times the votes cast against the resolution). Some specified disclosures like total numbers of stock options, identification of classes of employees, etc. have to be made in the explanatory statement annexed to the notice for passing of the resolution.

- A separate special resolution has to be passed for grant of option to employees of subsidiary or holding company or if grant of ESOPs to identified employees in a year exceeds one percent of the share capital.

- The Board of directors needs to disclose certain details of the Employees Stock Option Scheme in the Directors’ Report for the year.

- The company is required to maintain a Register of Employee Stock Options in Form No. SH.6 and the particulars of ESOPs granted by the company have to be recorded in this register forthwith. The Register can be maintained at the registered office of the company or at any other place approved by the Board. The entries in the register have to be authenticated by the company secretary of the company or by any other person authorized by the Board.

Restriction on ESOPs

- There shall be a minimum period of one year between the grant of options and vesting of option.

- ESOPs granted to employees can not be transferred to any other person.

- ESOPs cannot be not be pledged, hypothecated, mortgaged or otherwise encumbered or alienated in any other manner.

- The employer has the the freedom to specify the lock-in period for the shares issued pursuant to exercise of option.

Treatment of ESOPs on resignation, termination, death, etc.

- In the event of death, the option vests in the legal heirs or nominees of the deceased.

- If the employee suffers permanent incapacity while in employment, all options granted to him shall vest on the date of permanent incapacitation.

- If the employee resigns or is terminated, all options not vested in the employee expires. However, vested options can be exercised subject to the terms and conditions of the ESOP Scheme.

•Laws are constantly changing, either

their substance or their interpretation. Even though every attempt is made to keep the information correct

and updated, yet if you find some information to be wrong or dated, kindly let us know. We will acknowledge

your contribution.Click here to know more.

•Disclaimer: This is not professional advice. Please read Terms of Use (more specifically clauses 3 and 4) for detailed disclaimer.